It can be challenging to introduce new technology to your clients and employees.

If you’re a technophile that doesn’t understand these problems, consider this: More than ten percent of U.S. adults don’t use the internet, and of those individuals, one-third don’t use the internet because it was too difficult to use, according to Pew Research Center. Meanwhile, nearly one-fifth of Americans do not own a smartphone, or have limited or no Internet access.

Despite the perceived difficulties, there are many benefits to adopting new technology. In this article, we will look at why you should adopt new tech, some challenges to client and employee adoption, and how to overcome those challenges to maximize your return on investment.

Why Adopt New Technologies?

New technologies can be a pain to introduce to clients and employees – so why rock the boat?

There are two good reasons:

- Remaining Competitive – Consumers have been flocking to new technologies that simplify finances. For example, Mint connects various bank and investment accounts, tracks spending across multiple credit accounts, and tracks net worth over time. Robo-advisors, like Betterment and Wealthfront, have even started to cannibalize parts of the wealth management industry. It’s important to get out ahead of these trends to remain competitive and relevant to clients.

- Improving Operations – Enterprise technologies can help streamline and improve your internal operations, from lead generation and prospecting to rebalancing client portfolios and tax loss harvesting. These technologies can help you save time and focus more on building meaningful client relationships rather than getting bogged down in administrative tasks that are better suited for computers anyway.

There’s also strong evidence that new technologies can have a meaningful impact on your top- and bottom-line performance.

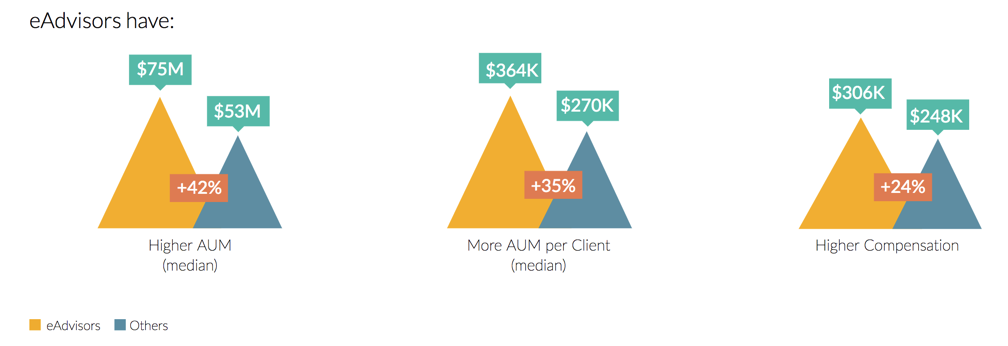

Fidelity surveyed financial advisors in 2014 and 2016 and divided them into two groups – tech-savvy eAdvisors and other advisors – to quantify how technology helps advisors.

eAdvisor Performance Comparisons

After comparing their performance over the two years, researchers found that AUM was 42 percent higher, AUM per client was 35 percent higher, and advisor compensation was 24 percent higher for eAdvisors compared to their peers who aren’t up on the tech.

Challenges to Tech Adoption

New technologies are a great way to improve the client experience and streamline existing operations to maximize your performance, but there are always challenges to selecting and implementing these technologies.

These challenges typically fall into three categories:

- Technology Selection – You’ve probably seen thousands of different technology solutions for advisors, but how do you choose the best options for your business? When researching technology solutions, it’s important for employees and clients to be involved in the decision-making process, but you should take a more careful approach than simply asking them what they want to see. Otherwise, you could end up selecting technologies that aren’t addressing real problems.

- Client Training – Many clients find portals, mobile apps, and other technologies to be a convenient way to manage their finances, but others find it stressful and/or challenging to learn yet another new technology. This may put you in the position of being tech support for your clients who aren’t in step with the technology. At the same time, it’s important to set the right expectations for adoption at the start. You will never see 100 percent of your clients adopt a new technology; 50 percent may be a more accurate target.

- Internal Adoption – Financial advisors that adopt firm-wide technologies may have trouble getting buy-in from their employees. For example, CRM solutions require every interaction to be logged to provide real value, which can be challenging when only some employees are committed to using the platform. Employees must also receive the proper training to ensure that they’re using the technology correctly, as inaccurate or inconsistent data could render the entire technology useless.

Overcoming These Challenges

Selecting New Technologies

The biggest mistake that many financial advisors make when selecting new technologies is deciding entirely based on client or employee suggestion rather than doing the research themselves. While this seems logical on the surface, it could easily send you down the wrong path.

A better approach is asking clients and employees about their problems and challenges and then selecting new technologies that tackle these issues.

Some questions to ask at various stages of the process include:

- What are some of the biggest challenges with financial planning?

- How do you manage your sales pipeline?

- How do you look at your complete financial picture?

- We’re considering introducing X to solve some of the challenges that you mentioned. What do you think? Would it help solve those challenges?

- Did we solve the problem that we set out to solve with that new technology?

Client-Facing Technology

The most important part of training clients on new technologies is understanding their problems (see above) and developing a clear communication plan.

Clear communication strategies focus on two or three benefits and provide simple instructions for using the new technology. Often times, it makes sense to set up and educate new clients as part of the onboarding process. You might help your clients set up and log in to their client portal, as well as download a mobile app during an in-person onboarding meeting. It may also help to create written or video tutorials, or even a knowledge base, to help clients in a self-serve fashion.

When rolling out the technology, consider telling only small groups of clients at a time. That way, you can quickly identify any problems without having 40 or 50 clients beating down the door with problems at the same time if something goes awry.

At Wealth Access, we walk your clients through the tech adoption process for you, so you can focus on higher value work and know that the process will go smoothly. This can save you a lot of time, especially if you have a lot of clients that you’re bringing up to speed.

Internal Software

The training process is a lot more straightforward with internal enterprise solutions. Oftentimes, enterprise software providers offer training programs designed to help you encourage employee adoption and maximize the usage of features.

For example, Salesforce’s Trailhead offers free guided learning paths designed to help people level up their skills, ranging from advanced administrative features to using formulas to improve workflow. Other organizations may offer in-person or virtual training for employees or a set number of tech support hours each month.

Salesforce Trailhead Courses

After implementing a new enterprise solution, it’s important to ensure that new employees are properly trained as part of their onboarding and everyone is held to the same standards when it comes to using the technologies in their daily or monthly workflows.

The Bottom Line

These days it’s crucial for financial advisors to be up on the latest tech. Consumers prefer web portals and mobile apps, and enterprise technologies are critical for advisors to remain competitive.

Encouraging clients and employees to adopt new technologies can be an intimidating process. By following the steps outlined in this article, you can ensure a smooth adoption of new technologies and maximize the long-term return on investment.

Schedule a demo with Wealth Access today to see how our client portals and mobile apps can improve your technology offerings.